A Market Timing Report based on the 4-08-2016 Close, published Saturday April 10th, 2016

I deliver focused comments on the markets. These are supplemented with “Tweets/StockTwits” (see links below).

1. SP500 Index: We are falling back from the yellow down trend line. If that trend is violated to the upside, we will likely see a Bull run back to the prior top or beyond. Earnings should be in the Bulls’ way this quarter. If they are not, we will re-top quickly. The punchline is that real GDP growth is supposed to be near zero in Q1, which I detail a bit further in my interest rate comments below.

SP500 Large Cap Index (click chart to enlarge; SPX, SPY):

Stocks are vulnerable to a pullback.

Sentiment is somewhat more Bullish this week among individual investors (AAII.com), though definitely still not at an extreme, with the Bull minus Bear spread at 10.7% this week (Bulls 32.2% and Bears 21.5% with Neutrals a Bullish 46.3%). See comments from three weeks ago on why that Neutral number is Bullish.

Please keep up to date at Twitter and StockTwits: See my messages on Twitter® Follow Me on Twitter®. Follow Me on StockTwits®).

2. U.S. Small caps are STILL above the 1040.47 level that for me defines a Bear market transition point, but small caps appear to be rolling over ahead of earnings. A break back below 1040.47 will indicate a resumption of the prior Bear market in small caps and would be a very negative sign for the entire U.S. market. GAAP earnings of small caps are negative for the trailing 12 months. Breaking above the yellow line instead would be a very Bullish sign. I doubt that it will happen prior to a move to the downside.

Russell 2000 U.S. Small Cap Index (click chart to enlarge; RUT, IWM):

Small caps turning over.

3. Gold: GLD fell back and tested the 50 day moving average, and has held up well following a powerful rally in February. The main threat to further progress is the U.S. dollar rallying from here. Typically gold only rallies with the dollar in times of panic. The dollar is back testing prior lows and could bounce. A dovish Fed could keep the slide going however. The hesitation in gold is likely due the market believing that the Fed will become even more dovish.

Gold ETF (click chart to enlarge the chart; GLD):

Gold rally holding up well after a high volume advance.

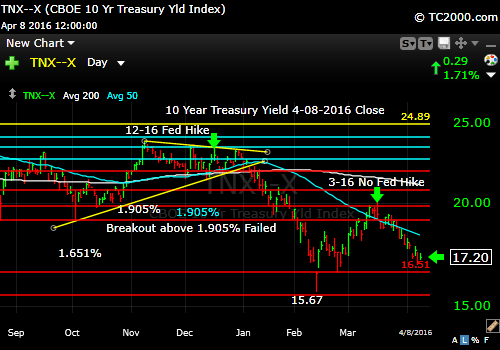

4. U.S. 10 Year Treasury Note Yield (click chart to enlarge; TNX,TYX,TLT,TBF): The failure of the Federal Reserve is seen on the chart below. They hiked rates and longer rates FELL. The opposite is supposed to happen in an expanding economy. This picture fits the revision of the Atlanta Fed of Q1 GDP down to 0.1% on Friday the 8th! It was 2.6% a few weeks ago, which shows the inability of the Fed to predict our economy’s future. The funniest thing about this is that the market is keying OFF OF FEDERAL RESERVE STATEMENTS!!! What a joke! The Fed has NO CLUE about what is happening, and yet the market seeks the Fed’s guidance.

Rates lead the Fed.

Stay with me throughout the week for the LATEST via the links to Twitter/StockTwits above. Feel free to comment, retweet etc. to spread the word.

Be sure to visit the website for more general investing knowledge at:

Standard Disclaimer: It’s your money and your decision as to how to invest it.

I thank Worden Brothers for the charting system I use to post these charts. If you want to know more about the charting system I use every day, go to my “Other Resources” page here: Other Resources It makes it much easier to follow along with me if you can see the charts and manipulate them on your own computer. It’s a great investment to have an excellent charting system. Check it out with a free trial at the link above.

Note that the newsletter is now CLOSED to new subscriptions: Join the Wait List to Join the Newsletter as a Loyal Subscriber, Opening again for the July 3rd issue. If you join and don’t read the newsletter, you will be deleted. Why? I don’t publish to non-readers as other newsletters do. I surround myself with committed people who value what we are doing. Stay tuned here in the meantime and follow all the action via the Twitter® and StockTwits® links above.

Copyright © 2016 By Wall Street Sun and Storm Report, LLC All rights reserved.