A Market Timing Report based on the 12-014-2018 Close, published Saturday, December 15th, 2018…

I deliver focused comments on market timing once a week. These are supplemented with daily “Tweets/StockTwits” (see links below).

1. SP500 Index Market Timing (S&P 500 Index®; SPY, SPX):

There are a lot of issues being faced by the weak market we’re experiencing. I count eight key issues.

1. Data on holiday sales. Data from aerial surveys of malls look decent per a report aired on CNBC, and U.S. retail sales were still OK in the last reading on Friday. As it stands, the Federal Reserve is “messing with Christmas” by continuing their stance of hiking into global economic slowing. Not smart! Many retail businesses do the vast majority of their sales in the 4th Quarter.

2. A Trump Xi Trade U.S. agreement with China within the 90 day period with the clock running since the G20 meeting.

China lifted some auto tariffs that are not that important numerically, but it was at least one positive in a sea of confusion. At least things did not become even worse this week. It would be great if the purveyors of contradiction in the Trump administration could simply close their traps! They did quiet down finally – let’s hope they stay silent unless they have positives to share in ONE VOICE!

3. U.S. interest rates staying relatively low, but not breaking too low (which hurts financial stocks).

I said last week: “Rates have moved down off the peak of 3.248% in the 10 Year Treasury Yield since Nov. 8th and now look ready to perhaps find support at the summer lows of around 2.80% and bounce.”

That’s about what they did. Rates bounced from 2.825% on Monday.

If rates drop to new lows below 2.80% or so, it will likely be paired with U.S. equity markets hitting fresh new lows.

What will the Fed do on December 19th at the end of their next FOMC meeting? This week the CME Group says the market is now only 76.6% sure vs. 71.5% sure last week that the Fed will hike 0.25%, whereas it was above 90% previously. A significant number of investors could find themselves “offsides,” as 23.4% of the market will be disappointed by a hike in December!

Volatility around the next rate decision is likely, given the percentage of potentially off-sides investors reflected in these odds.

As last week, I believe the market would rally on “no hike in December,” because it will be the clearest recognition that the Fed recognizes the slowing in the global economy is now impacting the U.S. and “going slower” on hikes would be better than risk adding a further drag on the economy.

Here is my full handicapping of the possible results of the FOMC Meeting ending Dec. 19th:

1. If the Fed does nothing (leaves rates unchanged) the market could rally based on their “finally getting it,” that the entire world is now in a growth slowing phase. The greatest bounce in stocks would occur on this news IMO.

2. If the Fed hikes 0.25% and says it will likely pause or something that is clearly dovish, the market could bounce as well, perhaps not as much.

3. If the Fed hikes 0.25% and does not make clear dovish overtures to the markets, the SP500 Index could move into the Big Red Wave.

4. If the Fed lowers rates by 0.25%, the market could collapse further in a vote of no confidence, because it would mean the Fed was more worried about the economy than many market players are. There is an upside risk with this choice of course as there is a common belief that you should not “fight the Fed.” I believe it would be temporary, however.

4. GDP growth is slowing. A reminder: “The Fed’s own numbers say growth of GDP is supposed to slow substantially into 2019 when GDP will be a mere 2.5% vs. 3.1% this year and by 2020 it will drop to 2.0% and then finally to their long run estimate of ‘longer run’ growth of just 1.8% by 2021. That’s a drop in GDP of 19.4% for 2019 and a drop of 35.5% for 2020 vs. 2018!”

This is the item that is very tough to shift, especially with the Federal Reserve hiking into slowing. If that changes, it will help. The other thing that will help is for the business cycle to reassert itself to the upside, something that could take several quarters without an additional fiscal stimulus such as infrastructure.

Should we spend more money we don’t have at a time when the deficit is already being blown out by Trump and the GOP with tax cuts? The deficit this year is running 17% higher than last year. Many Republicans will vote against a large infrastructure package or further tax cuts at this point, unless they have really lost their fiscal minds.

Bottom line? This “global growth slowing” period is a slow multi-quarter event, but we can monitor the economic data and analyst projections to decide when to add back equity exposure from our current lower level.

5. Oil staying low but not breaking to major new lows that would shut down drilling operations. Between OPEC cuts and robust U.S. production, the price of oil has languished near $50. It would help the market if oil prices stayed above $50 in jobs and financial stability terms.

6. Stability among tech stocks would help. Tech has been a bad sector for investors since the Sept. high in general terms. Stick with the exceptions, but be careful not to give back all your profits. XLK, the tech spider ETF, is testing near the higher April 2018 low.

If you are ahead 30% for example and allow a 10% loss from that, and then say, “Well it will probably bounce” and it then goes to a loss of half of the gain, meaning to a 15% gain, and then you say, “Well, it must bounce now,” and it then drops to a 5% gain…you get the picture. Decide on how much of your gains you are willing to give up and then stick to that number.

Sometimes paying taxes is cheaper than allowing your entire profit to dissolve away to nothing. Rebuying a stock higher is cheaper than if you “sell low.”

7. Impeachment and possible Senate trial risk for President Trump. Michael Cohen’s story is going to be corroborated, it seems, by David Pecker’s story in implicating President Trump in at least two crimes involving campaign finance laws. Yes, they are crimes despite the disinformation spewed by Trump claiming they were not crimes. Sometimes he is simply off the wall ridiculous in his outright lies to the public.

As I said on social media this week, our President appears to be a criminal. That’s a new event in evidence terms. This raises the risk of impeachment and another further drop in the stock market in my view. He does not have to be convicted by the GOP controlled Senate for the markets to drop substantially more. To prepare yourself, review, if you have not already done so, my Post on the Clinton Impeachment Market Decline.

I’ll stand by this from last week: The market would react even more negatively to Trump’s removal from office through a Senate conviction, but that is unlikely if there was no collusion with Russia. And yet, even after an additional decline, the market would then recover as Pence = Trump more or less.

8. U.S. Government Shutdown on Dec. 21: Remember that under Trump, the government shut down briefly from Jan. 20-21 2017, and a funding gap occurred the first part of the day of Jan. 9th of this year. Reagan had three shutdowns lasting a day or less. Clinton had two lasting five and 21 days. Obama had one lasting sixteen days in Oct. 2013 over funding of Obamacare (ACA).

Shutdowns are not the end of the world, but the market certainly does not need this aggravation during the busiest shopping period of the year. This is something Trump can easily compromise on with the Democrats, and he will be blamed for it, if it happens. He even said he’d accept the responsibility for it!

I suggest you contact the President and your House Rep. and two Senators via these links to urge them NOT to shut down our government: House and Senate. In many cases, you can simply leave a message with your comment or opt in to speaking with a staff member to leave your opinion. They do respond to public input. Send tweets to @POTUS and @WhiteHouse as well.

Now let’s check in on two “Canary Signals” we’ve been following:

“Intel-igent Market Timing Signal” (Intel; INTC): Negative, but now outperforming the SP500 Index. After rising in late October, it has been consolidating, while the SP500 Index has fallen lower.

Still, only a rise above 50.60 would change the current picture of a down trend since the June high. (Reminder: INTC was/is our “tell” on 2nd half earnings in tech as noted HERE.)

Bank of America (BAC) Market Timing Signal: Not Negative – Even More Horrendous than Negative. It fell to brand new recent lows this week. Financials broke the October low. This adds major risk to the overall market, which is why a rise of rates back up toward 3% would actually be welcome by the overall market (and hated by interest rate sensitive stocks like housing) as long as it does not occur too quickly.

There is a flurry of technical analysis this weekend trying to discern where the current market fall will stop. I’ve told you before, that’s a fool’s game. You have to handicap the future performance of company earnings and revenues, decide whether that is impacted by various policies and the above list of 8 issues the market faces, consider the rest of the world and its trajectory, etc. etc. etc.

I’ve shared with you the “secret” that you cannot possibly pick a “target” based on valuation, because markets often go higher AND lower than they should based on valuation, and furthermore, slowing can beget more slowing as we’ve seen as Ex-US slowing has infected the U.S. economy that most everyone believes is headed lower in GDP growth terms. That means whatever the analysts come up with today, they’ll have to downgrade in three months with the next set of analyst earnings projections.

What You Could Consider Doing

You may not sell until the next bounce or next breach of the SP500 Index for example, but it’s never too late for YOUR money to make strategic decisions and lay out your plan on paper or in a file! It will help you think more clearly to write it down or type it up!

- Lower your exposure and protect profits as close to what appear at the time to be highs in the market as slowing growth kicks in. That’s what I’ve been doing repeatedly at each market top. I coined the term “Passive Shorting” for this and you can read about it HERE. And then I add back exposure on the lows to play bounces, but in between I would suggest you also began to …

- Lower your “Top Level of Exposure During a Correction/Bear Market” (the SP500 Index is NOT yet one by my “New Rules“), while still playing bounces. You would optimally lower your exposure level at the tops or just off them, on a breach of trend for example. In other words, instead of going from 100% exposure at the top to 80% exposure and moving back to 100% exposure at a perceived bottom, you add back only 10% perhaps moving to 90% exposure as your “Top Level of Exposure,” during a correction until conditions change (the economy accelerates for example).

I’m now at roughly 72.5% exposure vs. the exposure I would normally hold during a solid Bull market. I’ve been adding near the current low, having sold exposure at the last high on 12-03, but not raising my exposure level back to 100% certainly until conditions change. Yes, sometimes I sell or buy exactly when I should as on Dec. 3rd. At other times I’m off by a day or two or more. Back near the first 2015 low in the SP500 Index, one of my buys was off by 2 days and another was off by 3 days. The market fell to yet another lower level on a breach during Flash Crash II in August 2015. I bought again even closer to the early 2016 low, but not at the low.

The key is this: you don’t have to buy the exact low to profit from a decline, as the U.S. market, in the end, goes up, not down as its major trend, at least until the United States ceases to be the world’s leading economy. (It’s no wonder Trump wants us to have a level playing field with China. On that, I agree with him.)

Individual stocks go down, yes, and dramatically so, and even disappear from the indexes, as GE has shown investors, regardless of the prior long term reputation of the company.GE is now down about 58% YTD. It’s out of the Dow but still in the SP500. Eventually it could be broken up and sold off into companies too small to be included in the SP500. This tells you indexes are in a way still “managed,” because they have to dump the losers when they fail to meet the criteria for the index any longer.

Let’s review where the markets are relative to the start of a Possible Big Red Wave as I’ve called it…

- The SP500 Index must hold the 10-29-18 intraday low or thereabouts. Remember, tests of levels often exceed them, and if the test is successful, a bounce ensues. For SPY, that is 259.85. For SPX it’s 2532.69. For SPX, the close was 2599.95 vs. the May low of 2594.62 and the Oct. low of 2603.54 and the Feb. low of 2532.69. To join the small and mid caps, the SPX would have to fall another 2.59% just to reach the Feb. low, which is why everyone is looking at, no staring at, these May and February lows “hoping” one of them will hold, because…

- Midcaps (IJH), which I said must hold the Oct. low, essentially at the February low, are now broken. The February low was 1770.19 and we’re at 1732.81 at Friday’s close. The Midcap index is -2.12% vs. the Feb. low. And misery loves company, so…

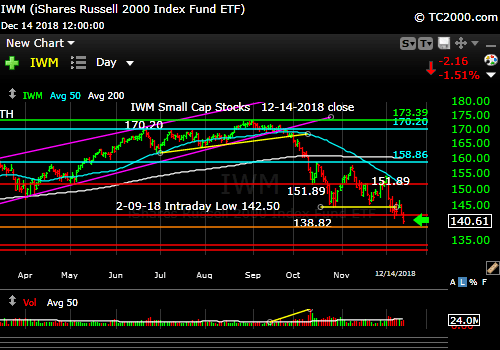

- Small Caps which I said must hold the February low, which they were barely above as of last Friday’s close are now BELOW that low of 1436.43 for the Russell 2000 Index (RUT) or 142.50 for IWM. The closes were 1410.81 and 140.61, respectively. The RUT is now 1.79% BELOW the Feb. low and IWM is 1.33% below its low.

If the small and mid caps are in fact leading the way as they did at the start of this downdraft, the Big Red Wave may be about to start for the SP500 Index, because it’s begun for the small and mid caps.The optimistic view would be that small and mid caps are higher risk, so they are testing lower than the SP500 Index, which will save the day by holding the February low.Without a positive catalyst or preferably the alleviation of more than one of the current issues listed above that are facing the markets, the market could simply continue lower.The Federal Reserve statement at 2 pm Weds. and the dog and pony show at 2:30 pm could be such a catalyst.

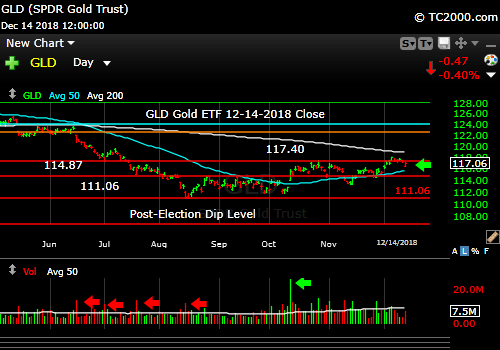

- Gold: I said last week gold must pull back as rates rise again with the dollar starting Monday. I also said the financials should be helped by that and they were not, which is a problem for the market. However, my prediction held. Dollar was up, rates are off the lows, and gold has eased a bit.

If positive catalysts can be conjured up by the Trump trade team, no government shutdown, and a dovish Fed, the market could bounce from here. Two of those could be enough. The Fed alone could be enough to delay the next sell-off to 2019. I reviewed the possible “Bounce Levels” HERE (scroll down and you’ll see the list) previously.

If the SP500 Index breaks support and follows the breaches by both small and mid caps this week, the “Big Red Wave” I described three weeks ago HERE could begin. That would drive massive buying of U.S. Treasuries, driving rates down even further. What will I do in that case? I will be lowering my exposure to no more than 60% of my usual maximum equity exposure for a Bull market worldwise if the SP500 Index decends into the Big Red Wave. I may do it in steps to avoid being whiplashed by a 1-2 day breach of the lows as happened before.

I pointed out this week, December crashes through major support are virtually unheard of. But maybe Trump can make things even worse than he has and create the first such December crash since 1970. I went back to there and found two instances in which:

- December 1973: There was a test in Dec. of the 1971 low that succeeded followed by another major decline in 1974. However, we were in recession from 1973-1975, which is not the case now. We cannot assume a January 2019 rout. In any case, the rout did not come in December!

- December 2000: In December there was a swoon below major support and the year ended “on the edge.” There was a bounce but the year did not end above support and 2001 was even worse after a short rally as I described HERE in my StockTwits Market Timing Room. Remember that 2001 was a continuation of a massive Bear market for the SP500, but even more so for tech stocks that went down 78% from the highs.

Will this be the first time since 1970 (which was as far as I looked) that the market crashes through obvious support and just keeps falling?

The odds say no, but as I said in the room, it could be different this time, and in 2019 if there are weak Q4 numbers and projections reported in February the market may go over the edge.

Keep up-to-date during the week at Twitter and StockTwits (links below) where a combined 33,802 investors are following the markets with me…

Follow Me on Twitter® Follow Me on StockTwits®.

SP500 Large Cap Index (click chart to enlarge; SPX, SPY):

Will it hold the February low or descend into the “Big Red Wave”?

Survey Says! Sentiment of individual investors (AAII.com) showed a Bull minus Bear percentage spread of -27.97% vs. +7.44% the prior week. There has finally been enough of a washout of Bullish sentiment to allow for a bounce. But sentiment has room to be even more negative. It says the SP500 Index could hold February support is the best I can say. Not reassuring, again, without distinct positive catalysts like the Fed being clearly dovish.

| AAII.Com Individual Investor Sentiment Poll | ||

| Bulls | Neutrals | Bears |

| 20.90% | 30.23% | 48.87% |

| Thurs. 12 am CT close to poll | ||

2. U.S. Small Caps Market Timing (IWM): I covered the key points above. Not a place to add unless you are just averaging in blindly.

Russell 2000 U.S. Small Cap Index (click chart to enlarge; IWM, RUT):

A Broken Chart

3. Gold Market Timing (GLD): I said last week: “So for the very short term, I’ll wait to add more GLD.” That was correct. I have no gold trades on for now. Just insurance (I’d suggest 5% of investable assets as most do; remember gold yields zero and makes us paper money only when rising! If you own none, average in over time or buy the lows and sell the highs if you like.). I have to see more strength and wait for rates to retop out to buy back into a trading GLD position.

The Gold ETF (click chart to enlarge the chart; GLD):

Gold slipping on higher rates and higher dollar.

4. Interest Rate Market Timing – U.S. 10 Year Treasury Note Yield (TNX):

Two weeks ago I said: “If they [rates] continue to fall as the stock market rises, beware! That’s not how it is supposed to work in a recovery. It means the recovery is false. It means the stock bounce will be limited.”

I said last week: It’s critical that rates bounce early next week, preferable on Monday.

They bounced on Monday and should continue higher UNLESS the Fed turns more dovish on Weds and especially if they don’t hike (not likely per CME Group – see above).

Check out the “Market Signal Summary” below – after you review the following chart…

U.S. 10 Year Treasury Note Yield (click chart to enlarge; TNX, IEF, TYX, TLT, TBF): (Ignore the caption saying “Lower Still. Ready to bounce?” – it did bounce higher!)

Rates reach a prior low and bounce on cue.

Now let’s review three key market timing signals together….

Do not use these signals as a trading plan. They are rough guidelines. I currently share my own moves on social media (links above).

MY MARKET SIGNAL AND TREND SUMMARY for a Further U.S. Stock Market Rally with Real GDP Growth (“Real” means above inflation):

RED RED RED this week.

Stock Signal RED for a further U.S. stock market rally with a BEARISH SP500 Index trend. (The Signal here is based on the small caps, and I’m sure you know their trend is also Bearish!)

The VIX (which relates to SPX volatility) closed at 21.23 this week vs. 23.23 last week , which remains Bearish. The trend is still UP and That is still a high VIX. The VIX did reclaim 22.97 and must avoid rising above 23.81, which would embolden the Bears in a big way. The close Friday was below the up trend line of VIX (now at 22.88). These numbers change daily. The next Bear target above 23.81 is 25.94.

Further VIX Bull Targets: 20.34, 18.18 to 18.10, 17.24, 16.86, and 15.95 to create a new recent low. The ‘Bull Nirvana Target’ is our VIX # of the Year: 13.31.”

Five weeks ago I said: “The Bears need to take out the 26ish top that was tested once again this week for the market to go into another leg of decline. If they do it soon, it COULD still just last a day or two.” The last test of that was on 12-06 at 25.94.

As before, VIX 28.84 is the Bear target for Armageddon (another big chunk of losses driving SPX down significantly lower). Just moving above 26 could do it however.

Gold Signal YELLOW for a further U.S. stock market rally with a NEUTRAL Gold Trend. It has slipped back into the prior consolidation band. That’s a near term negative. See above for more. A gold rally, if strong, would be a sign of global financial panic if seen with a strongly rising US dollar.

From before: “Remember GLD is being used as an indicator for the ECONOMY here.”

Rate Signal RED for a further stock market rally with a BEARISH 10 Year Yield Trend. The trend is still down despite the bounce. Watch the oil price too. Higher oil tends to mean higher rates.

As for much higher rates and their possible impact, I said previously: “All heck would break loose for equities if TNX lurches above 3.248%, particularly if the rise is rapid. You buy long dated Treasuries as close as you can to 3.248% on the 10 Year Yield TNX (IEF, TLT, etc.).”

I previously warned about the Fed tightening process: “This level of the 10 Year Treasury Yield, which is too high for current conditions as explained HERE, will eventually slow the economy.”

Sept. 28th issue: “A rapid push higher in rates would mean trouble for stocks, as occurred in early 2018. That’s what I call ‘Rate Shock.'” The period of rising rates in early October was #RateShockII as I called it.

Thank you for reading. Would you please leave your comments below where it says “Leave a Reply”… or ask a question or report a typo…

Pay it forward by sending the link to MarketTiming.Blog (that link will immediately connect them to this webpage) to a relative or friend. Thanks for doing that.

Be sure to visit the website for more general investing knowledge at:

Standard Disclaimer: It’s your money and your decision as to how to invest it.

I thank Worden Brothers for the charting system I use to post these charts. If you want to know more about the charting system I use every day, go HERE. It makes it much easier to follow along with me if you can see the charts and manipulate them on your own computer. It’s a great investment to have an excellent charting system. Check it out with a free trial at the link above. I am an affiliate of Worden Brothers, though oddly I’ve never been paid a cent by them. If you HAVE subscribed to their service, please send me a message. 😉

Note: I’ve updated my criteria for the equity signal for a further U.S. stock market rally to the following: GREEN = Bullish, YELLOW = Neutral, RED = Bearish. In other words, the colors tell you whether the signal supports the stock rally or not, while the Bullish, Neutral, and Bearish designations are about the trend.

A BEARISH trend signal does not mean we should not buy. A BULLISH trend signal does not mean you cannot sell some exposure. It depends on what is going on in the economy and how oversold/overbought the market is at a given point whether the Bearish signal is to be sold, sold on the next bounce, etc. and whether a Bullish signal is to be bought or if profits should be taken. A NEUTRAL trend signal does not mean the end of the Bull or Bear. It means to wait and look for possible subsequent entry points within the existing trend, Bull or Bear, but preserve capital if the entry fails. Our strong intention is to buy low and sell high. By the way, I will keep showing the prior orange “Trigger lines” in the charts for now as reference points only; they have historical value for us from the post-2016 election period.

Copyright © 2018 By Wall Street Sun and Storm Report, LLC All rights reserved.