A Market Timing Report based on the 03-15-2019 Close, published Saturday, March 16th, 2019…

I deliver focused comments on market timing once a week. These are supplemented with daily “Tweets/StockTwits” (see links below) and comments in the “markettiming” room on StockTwits.

1. SP500 Index Market Timing (S&P 500 Index®; SPY, SPX):

This was a Mini Bear Market as I explained in my “New Rules” (Oct. 26, 2018 post; the total dive top to bottom in the SPX was about 20%), but this week, actually on Friday, the SP500 Index finally climbed over the three prior Lower Highs of October, November, and December. Some may claim the market needs to make a brand new all time high (ATH) to be called a Bull again, but that’s not my view. I recommend using the SP500 Index vs. SPY in making this judgment, since dividends effect the latter.

Is a new higher high for one day enough to say the Mini Bear is dead? No. It takes up to 3 days, as traders know, to confirm a move, but the way machines trade these days, that can mean leaving several percent on the table if you wait. So I didn’t wait. I added what amounts to about 3.6% of additional exposure vs. my usual maximum 100% exposure level (which is NOT 100% stocks; adjust to taste is the point; follow my equity exposure level as I buy/sell on social media [links below]). My intention is to add further exposure higher or lower. I have no need to sell this exposure should the market turn down again. If you add when you are already invested to the gills, you may need to sell to preserve capital.

To me, this is a fledgling Bull Market, but what don’t I like? For one thing, the NYSE based Advance/Decline % Line (T2100) that I follow on proprietary software, shows a failure to make new highs despite the SP500 Index breaking out above the triple top target levels. That means the move on Friday could be a head fake. There must be at least consolidation at a minimum (sideways move), and then follow through to keep the Bull ball in the air. Also, see “small caps” below, another warning sign.

And earnings could weigh on the market when Q1 2019 results start coming in during the first half of April. Once again this week, earnings predictions for 2019 are worse for the entire year and for Q1 2019, but seem to have stabilized for Q2 and Q3 with another tick down for Q4. The vast majority of SP500 companies had reported Q4 2018 earnings as of last week. These data are from FactSet, and the full FactSet PDF report will open HERE, and this is their site.

I have updated the matrix of numbers shown over the past several weeks. These are the SP500 Index Earnings and Revenue growth (or lack thereof) numbers predicted as of the Feb. 2nd vs. the Feb. 15th vs. the Feb. 22nd vs. the Mar. 1st vs. the Mar.8th vs. the Mar 15th close by FactSet, from left to right…

“For Q1 2019, analysts are projecting a decline in earnings of -0.8% -> -2.2% -> -2.7% -> -3.2% -> -3.4% -> -3.6% and revenue growth of 5.7% -> 5.3% -> 5.2% -> 5.2% -> 4.9% -> 4.9%.

For Q2 2019, analysts are projecting earnings growth of 1.6% -> 1.0% -> 0.7% -> 0.3% -> 0.2% -> 0.1% and revenue growth of 5.1% -> 4.7% -> 4.7% -> 4.8% -> 4.5% -> 4.6%.

For Q3 2019, analysts are projecting earnings growth of 2.7% -> 2.4% -> 2.2% -> 1.9% -> 1.7% ->1.8% and revenue growth of 4.9% -> 4.5% -> 4.5% -> 4.6% -> 4.5% -> 4.4%.

For Q4 2019, analysts are projecting earnings growth of 9.9% -> 4.8% -> 4.5% ->4.1% -> 3.9% and revenue growth of 6.0% -> 4.9% ->4.9% -> 5.1% -> 5.0%.

FactSet says (showing this week and the prior two weeks for this data) …“For CY 2019, analysts are projecting earnings growth of 4.1% -> 3.9% -> 3.8% and revenue growth of 5.1% ->5.0% -> 4.9%.”

Again, I’d say the 2019 full year guesses are overly optimistic as the earnings growth number for 2019 cited does NOT match the quarterly data above it.

One highlight of their report this week, which is worth your time, is that Energy, Healthcare, and Communications Services had the highest percentages of buy ratings. It’s important to look deeper into the data, because many drug companies are not expected to do well, while those who directly provide health care are presumed to be among the winners (see my comment in last week’s brief on the Pharma sector). With lower interest rates and potential for big growth potential, biotech is considered a buy by many (multiple concordant sources). The biotech ETF IBB is one way to play that.

Here’s a Brief Review of the Market Risks at Hand:

China Deal Risk: There is going to be a “big, beautiful deal.” It’s taking longer than most had hoped, but this is an attempt to correct years of abuse by the Chinese. If Trump walks away, it would greatly upset the market however.

Mueller Risk: We are STILL told his report is imminent, so the risk of a surprise is imminent. This is a coin toss for Trump himself as I’ve said, but not for players like Don Jr. I’d say they are still very much at risk, but the market could care less about them.

2020 Election Risk: Read my comments on this HERE. Remember, I’m an independent who seeks the best ideas of both parties. I’ve voted for both parties’ candidates, even in the 2018 midterms. In my view, the election of a liberal Democrat would be an immediate, intermediate and longer term disaster for the U.S. markets. Luckily, so far, our country does not support a shift to socialism/communism, which has proven severely lacking on the innovation side of things.

Many of the greatest and most innovative companies are in the United States. They mostly are not in Europe, China, India, or even Japan. They spend their time attacking our great companies and fining them. China has kept U.S. tech companies from entering China, so they could rip off and essentially duplicate Amazon, Google and other companies from within. The number of people you have does not create innovative thinking. China has only recently started to understand that it must innovate to lead. Hence the huge AI research effort. Trump is right that China must stop ripping off U.S. tech immediately. I give him credit for that.

Given then that the failure of any socialist candidate is likely, even if the more liberal candidates push a moderate Democrat strongly to the left in their platform, we could easily end up with Trump as a two term president. Sanders is dead-on-arrival as he will scare seniors half to death when they find out the lines to see their doctors will run out the front door and around the corner. (I do agree all human beings deserve decent healthcare, and the underprivileged deserve a break on college costs, but how we get there is another thing. Zero loans? Why? I completely disagree with Sanders that all kids should go to college for free. Many should have a vocational education, not a general and impractical BA from a college. Beer sales would definitely go up under a Sanders Free College program. Buy BUD, if you think he’ll win!)

The only type of Dem who can beat Trump cleanly would be Biden, or Klobuchar in theory only, because she’s not getting early traction that proves her candidacy as viable. John Kasich was the same sort of candidate. Both of them are probably very good people to have as President, but a candidate with little charisma is not going to be elected. Nice, honest, intelligent, and self-aware is not enough unfortunately.

Our choice will likely be Biden vs. Trump (if Mueller has nothing big on Trump). Biden’s grief process after his son’s death from brain cancer is what gave us Donald Trump. If Trump is booted (not in the cards at this point) Biden would beat Pence by 10-20%. Pence is old school and barely likeable. Voters like “likeable.”

By the way, a President Biden may end up being indebted to people far more left than he is and do things the market may dislike, especially a roll back of tax cuts for corporations and individuals. The stock market would correct strongly if that were done IF the net effect were a fiscal drag on the economy. If they take from the rich and give to the middle class and keep the corporate rates low, that may not happen.

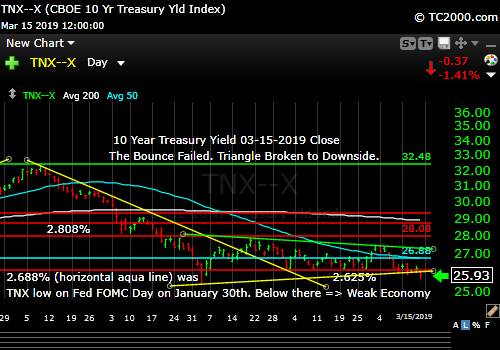

Fed Rate Hike Risk: Lower this week as rates have fallen. If TNX is below the January Fed day low of 2.688%, I consider it Bearish for rates (bonds higher, rates lower). As I said last week, “The risk of a Fed hike with easing in China and Europe…is LOWER.”

Before we look at the chart, I’ll answer… Why did I also add on March 7th, after the market was down about 3%? Because pullback levels are not predictable except for short term moves, and it was my intention to take advantage of pullbacks in the rally when they appeared. It worked. We will see early next week whether the buy on 3-15 also worked.

Now take a look at the SP500 chart…. The orange lines are the 2017 up channel.

SP500 Large Cap Index (click chart to enlarge; SPX, SPY):

Will the rally continue higher now that we’re above the triple top?

Now let’s check in on two “Canary Signals” we’ve been following:

“Intel-igent Market Timing Signal” (Intel; INTC): Bullish. The low was 51.70, so it never got back down to the prior breakout level. Intel itself has warned about another weak quarter for Q1, so we will see if it can hold up through that report supposedly on 4-25-2019.

Bank of America (BAC) Market Timing Signal: Neutral and vulnerable to lower rates. XLF is still stalled below the 200 day moving average (mav). BAC is stalled too.

As I said last week, the “Only Way Up” is # 1 below.

- “Break out to new highs with SLOWLY rising OR stagnant interest rates. This is the ONLY way UP for the U.S. stock market.

I added the word stagnant, since that would also satisfy the stock market. My immediate Bear target if the rally folds, would be the Oct. low, which is now 7.76% lower from the Friday SPX close. We are just 4.19% from the prior intraday all time high (ATH). In that sense, a Bear would tell you the downside is greater than the upside. I would say they may be right in the short (a quarter or less) or intermediate term (a few quarters), but I doubt they are right in the longer term.

Now let’s go on to review investor sentiment…

Keep up-to-date during the week at Twitter and StockTwits (links below) where a combined 33,914 investors are following the markets with me…

Follow Me on Twitter® Follow Me on StockTwits®.

Join the Conversation in the StockTwits “MarketTiming” Room

Survey Says!

Sentiment of individual investors (AAII.com) showed a Bull minus Bear percentage spread of +1.36% vs. +10.64 last week. When sentiment falls as the market rises to test a top, investors are simply getting nervous as they see the market as being fully valued vs. that prior high. It also says “That is not THE top.” We have not been at exhaustive sentiment levels since I pointed one of those out just before the highly volatile Jan. 2018 correction.

The top is yet to come! There may be pullbacks still as we work through very negative earnings data for a few quarters (buying opportunities IMO), but the market will work its way back from any correction, as long as our economy does not slip further toward a recession.

| Bulls | Neutrals | Bears |

| 32.42% | 36.52% | 31.06% |

| Thurs. 12 am CT close to poll | ||

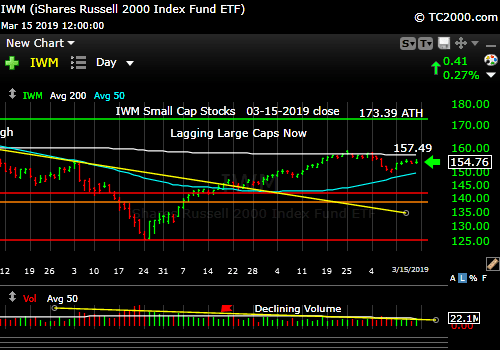

2. U.S. Small Caps Market Timing (IWM): Small caps are showing negative divergence vs. large caps. With the SP500 Index making new market timing highs, the small caps should be doing the same, but they are not! They need to rise soon and confirm the SP500 Index buy signal. Small caps led the market down from the Sept. 2018 all time high, and they could do it again right now. Note: I’ve added large cap exposure, not small, on the recent dip and again on the breakout of the SP500 Index.

Russell 2000 U.S. Small Cap Index (click chart to enlarge; IWM, RUT):

Small caps lag large.

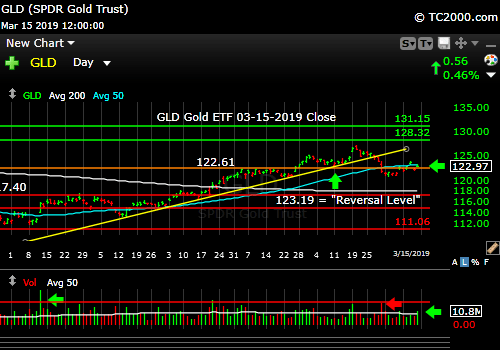

3. Gold Market Timing (GLD): GLD is now 0.80%, vs. 0.69% last week, above my sell point. Interest rates falling should be helping GLD more than it is. That’s a negative for GLD. The chart below shows you the reversal level I’d be following if you are trading GLD.

Why has the recent trend been damaged? What gold does NOT like is rising real rates, so if the Fed whiffs more inflation than it wants, that could pressure real rates higher. A proactive Fed means rates rising AHEAD of inflation, which means rising REAL RATES – the thing gold hates. Rising oil prices also often means higher rates. The gold market is signalling that the Federal Reserve is, as I’ve contended, at best going to “act neutral,” not dovish.

I’ll change my mind if we see the upside reversal noted in the chart below.

The Gold ETF (click chart to enlarge the chart; GLD):

Gold rally on pause still. Looking for a reversal UP.

4. Interest Rate Market Timing – U.S. 10 Year Treasury Note Yield (TNX):

TNX closed Friday at 2.593%, now below 2.688%, or what I am calling the “Fed’s gone dovish number.” It also broke the triangle (yellow line) to the downside. The Fed is actually neutral as I said, which is enough to move rates down a bit more than they were. If TNX were to make a brand new low, the stock market will likely enter a dip/correction, as that is NOT what is supposed to happen in a real recovery The Fed would have to move to an outright dovish position if that were to happen, at least in time they would.

Rates RISE in a recovery. Rates fall as the Fed moves to a dovish stance and keeps lowering rates as the economy falls off a cliff. That is not what is supposed to be happening. The rosy scenario is that rates are low because the Fed is dovish, and they’ll even cut rates to help the stock market stay up. They won’t cut rates if inflation is too high, as long as the stock market is not “doing badly,” which it definitely is not.

Check out the “Market Signal Summary” below – after you review the following chart…

U.S. 10 Year Treasury Note Yield (click chart to enlarge; TNX, IEF, TYX, TLT, TBF):

Rates fall below the recent range. Bullish for Treasuries and bonds.

Now let’s review three key market timing signals together….

Do not use these signals as a trading plan. They are rough guidelines. I currently share my own moves on social media (links above).

MY MARKET SIGNAL AND TREND SUMMARY for a Further U.S. Stock Market Rally with Real GDP Growth (“Real” means above inflation):

Stock Signal NEUTRAL for a further U.S. stock market rally with a Bullish SP500 Index trend. The signal here is based on small caps, as they often lead the market down. Small caps are signalling some relative weakness this week, but I’ll move the signal to neutral given the bounce over the last 5 days in small caps.

The V*IX (which relates to SPX volatility; * added to symbol to throw off the webcrawlers!) closed at 12.88 vs. 16.05 last week, which means the Bulls have reached “Nirvana.” That implies there could be more immediate upside for the SP500 Index.

There are now 7 Bear targets and the score is Bulls 7 to Bears 0. The targets are 13.31, 14.04-14.08, 15.04, middle point = [15.94-15.95 to 16.09], 17.06, 17.27, and 17.89.

The ‘Bull Nirvana Target’ is our V*IX # of 2018: 13.31.” (That # is target #7 for the Bulls.)

Gold Signal YELLOW for a further U.S. stock market rally with a NEUTRAL Gold Trend. What gold does mostly as I’ve written HERE is follow real interest rates. STILL HOLDS 3-15-19: G*LD has to rise above 123.19 on an immediate basis (* added to throw off the “crawlers,” as I don’t like being part of “consensus.”)

From before: “Remember GLD is being used as an indicator for the ECONOMY here.” If gold continues to rise, it means the market believes real rates will fall, which means the global economy is slowing. That would hurt U.S. stocks.

Rate Signal NEUTRAL for a further stock market rally with a BULLISH 10 Year Yield Trend. The only reason I am not chasing Treasuries here is that over the subsequent several quarters, inflation is predicted to tick up a bit. I prefer to be in short term paper (< 1 year) with my cash with that inflation outlook. Rates will rise slowly and so will the yield in short term Treasuries and money market funds. Of course, rising oil prices is also a reason to be cautious on the move to lower rates. I am calling rates NEUTRAL for the stock market rally, because the market likes lower rates. If rates fall to new lows (substantially toward 2.554% or lower), however, that will mean something else, namely a worsening economy, and stocks would likely react negatively.

I said weeks ago, “Watch the oil price too. Higher oil tends to mean higher rates.” WTI broke out again this week, closing at 58.36.

I previously warned about the Fed tightening process: “This level of the 10 Year Treasury Yield, which is too high for current conditions as explained HERE, will eventually slow the economy.” I said, “2.621% was the peak back in 2017 when stocks did best. Anything below that would be an improvement.” The close on Friday? 2.593%!

Equity buyers feel lower rates are better at this point, but that’s not true for financials, so avoid that sector for now.

As for much higher rates and their possible impact, I said previously: “All heck would break loose for equities if TNX lurches above 3.248%, particularly if the rise is rapid. Buy long dated Treasuries as close as you can to 3.248% on the 10 Year Yield TNX (IEF, TLT, etc.).”

Watch the rate at which TNX climbs if the current trend reverses. If it shoots up very fast, stocks will correct. In the Sept. 28th issue: “A rapid push higher in rates would mean trouble for stocks, as occurred in early 2018. That’s what I called ‘Rate Shock.'” The period of rising rates in early October I called #RateShockII. The next shock, I’ll be calling #RateShockIII.

Thank you for reading. Would you please leave your comments below where it says “Leave a Reply”… or ask a question or report a typo…

Pay it forward by sending the link to MarketTiming.Blog (that link will immediately connect them to this webpage) to a relative or friend. Thanks for doing that.

Be sure to visit the website for more general investing knowledge at:

Standard Disclaimer: It’s your money and your decision as to how to invest it.

I thank Worden Brothers for the charting system I use to post these charts. If you want to know more about the charting system I use every day, go HERE. It makes it much easier to follow along with me if you can see the charts and manipulate them on your own computer. It’s a great investment to have an excellent charting system. Check it out with a free trial at the link above. I am an affiliate of Worden Brothers, though oddly I’ve never been paid a cent by them. If you HAVE subscribed to their service, please send me a message. 😉

Note: I’ve updated my criteria for the equity signal for a further U.S. stock market rally to the following: GREEN = Bullish, YELLOW = Neutral, RED = Bearish. In other words, the colors tell you whether the signal supports the stock rally or not, while the Bullish, Neutral, and Bearish designations are about the trend.

A BEARISH trend signal does not mean we should not buy. A BULLISH trend signal does not mean you cannot sell some exposure. It depends on what is going on in the economy and how oversold/overbought the market is at a given point whether the Bearish signal is to be sold or bought, sold on the next bounce, etc. and whether a Bullish signal is to be bought or if profits should be taken. A NEUTRAL trend signal does not mean the end of the Bull or Bear. It means to wait and look for possible subsequent entry points within the existing trend, Bull or Bear, but preserve capital if the entry fails. Our strong intention is to buy low and sell high. By the way, I will keep showing the prior orange “Trigger lines” in the IWM and GLD charts for now as reference points only; they have historical value for us from the post-2016 election period.

Copyright © 2019 By Wall Street Sun and Storm Report, LLC All rights reserved.

Thank you David! Are we not a socialist country already? Congress passed and Trump signed a 900 billion dollar give away to the farmers in that tariff farm bill? The FOMC policy to support the stock markets is a social policy to support the middle class and rich! All US citizens are in some way benefiting from some form of social assistance. The tax cut for the rich should be rolled back and corporations should not pay zero taxes! I’m worried about the National Debt and the Republican ideas to address it are, cut the social programs that I’ve paid into for 40 years. The Republican Party is no longer conservative when it comes to spending, they just don’t like it when Democrats over spend. I can agree our country will not support a shift to socialism however we have to acknowledge our country is hooked on social programs! The people can’t have it both ways, accept social programs, you will eventually acknowledge what our country is.

I supposed you could say that, but not to the extent Europe is socialist and the “delta” is more important than the level. On the Fed, I agree completely. They reinflated both stocks and housing, and Bernanke and Yellen ignored the need of some for a decent savings rate. Powell is in danger of killing off the interest rate on savings yet again. The politics aside, because I wrote a post on “The Invention of Fiscal Lying,” both parties are to blame for the state of the U.S. balance sheet.