A Market Timing Report based on the November 22, 2019 Close, published Saturday, November 23rd, 2019…

I deliver focused comments on market timing once a week. These are supplemented with daily “Tweets/StockTwits” (see links below) and comments in the “markettiming” room on StockTwits.

I provide quite a bit of intraweek commentary, and if you don’t see it, you will miss out on quite a bit of context, so please click on the social media links below and have a read… Thank you as always for being loyal readers and interacting on social media with your questions and comments!

1. SP500 Index Market Timing (S&P 500 Index®; SPY, SPX): Investors were asleep again this week despite the Trump impeachment hearings. This weekend there is a report that one of the indicted Giuliani thugs is willing to testify that Rep. Nunes (Republican ranking member on Intel Committee) went to Europe to procure dirt on Joe Biden. So stay tuned, but from what we know now, “Teflon Don” is safe on the Senate side as he continues to convert negative energy from the left to positive energy among his base. Some may call his energy “positively negative,” but apparently it’s an acquired taste. The point is he uses the attacks as an energy source for his support and re-election. The small caps having been oscillating in a narrow range for 15 straight trading days! But something is about to give…one way (down) or the other – that would be UP.

Rates fell a bit more this week. They are a key that will determine which way important markets inflect, up or down. Right now they are above the trend established since the Aug. to early Sept. low, so the 10 year Yield is still in an up trend. At the same time, a breakout above 1.903% failed as I have reported.

The NY Fed now predicts Q4 GDP at 0.71%, the Atlanta Fed at an even more non-Trumpish 0.4%. That is abysmal and yet, the market could care less because the Fed is lowering rates….oh wait, they are in “Neutral” I believe Dave (that would be me) said last week.

Larry Kudlow promised us 3% growth, after he promised us 4% growth or higher from the tax bill which now has the 2019 deficit 26% above 2018 as I’ve shared. “Tinkle Down Economics” fails for the 3rd time. What is that expression? “Fool me once shame on you; fool me twice shame on me!” They don’t even cover the 3rd time of being fooled, so the average voter is in fact ignorant apparently, and has not a clue when they are being lied to. To cover all bases: Both sides/All sides lie. They just can’t help themselves, because they all want something for themselves, be it influence, power and stature for its own sake, money, or the crown of “Give Away Queen” and “Savior of Everyone,” which Elizabeth Warren will get if she wins (she won’t IMO). You see how truly politically independent I am? 😉

Let’s turn to the state of the market…

What would satisfy me that the Bulls are serious?

The Bull Market Health Score this week is still Bulls 2.5/Bears 2.5 vs. Bulls 4.0/Bears 1.0 last week. It’s a 5 point scoring system.

For each checklist item below, I give you the points scored as Bullish or Bearish.

1. New high? Bulls 0.5 Answer: Neutral. Stretched vs. trend, and also down vs. last week. But no break lower yet.

2. V*IX trend favorable? Bulls 0.5 Answer: Neutral. The VIX Game Score is Bulls 7/Bears 0 at a VIX of 12.34 (Friday close) vs. 12.07 the prior week, which is below my “Bull Nirvana” number, which is the 7th Score point. The Bulls lost the “bonus” VIX point that I used to refer to in my score. As Before: “The 2018 low was 10.17, so there is still room to fall. It was 8.56 in 2017, but earnings were better then and lots of growth was anticipated under the Trump tax cuts.” I said last week: “The VIX has to break 12.00 next week or else.” It hasn’t broken below 12, though it tried last on Fri. the 15th, and the market has made no progress, falling about 10 points for the week.

3. AD % Line in an Uptrend? (This is a proprietary stat; see base of report.): Bulls 0.5 point. Answer: Neutral. The close was 16,848 vs 16,888 last week. The number is down from where it was 16 trading days ago, so there has been no progress, even as the market has edged up a bit above trend. Last week: “It must make a new high next week or else.” No breakdown yet, as said, but no break to the upside in this parameter makes it “Neutral.”

4. Higher volume on Up Moves? Lower volume on Down moves? Bulls 0.5 point. Answer: Neutral. Volume has not been impressive on either the Bullish or Bearish side.

5. Is the “U.S. Index Matrix Signal,” as I call it, positive? Bulls 0.5 point. Answer : Neutral. Now it’s been a full FIFTEEN market days, and SAME: “small caps have not broken above the longer term range while mid caps have been holding above that level for 15 days – but not by much. The mid cap breakout did not reverse, but it also did not continue up with the large caps.”

Still true: A small cap breakout would mean the market upside is not done. On the other hand, with small caps holding below the top of the range for fifteen days straight, I would not be shocked to see a pullback begin. In July, the small caps traded sideways for 17 days and then rallied a bit, followed by 3 days of sharp downside (but only a small correction) on high volume. The midcaps did about the same thing. I doubt the market is going to rally for more than a news related pop, which could be followed by a correction (5-15% drop; scroll down to “New Rules” on my definitions HERE).

Even the impeachment hearings could not inspire either buying OR selling this week.

Let’s check in on the context around the price action of the market by looking at the current Market Risks…

We have some new earnings data this week…

Earnings Risk/Opportunity: what is shown are the projections in the FactSet 3-15-19 report followed by the reports from 4-12-19 through 8-09-19 with a skip of two weeks until the 8-30-19 data resumes the weekly data sequence (details HERE)… The larger arrows “—>” indicate 3 weeks of of omitted data in order to compress the data. NOTE: 96% of SP500 Index companies have reported. That was just 5% more than last week.

Hurrah! Earnings for 2019 are now projected to grow a whopping 0.1%! Please do not step on that green shoot! 😉 Note also though that Q2 2020 earnings growth estimates have finally stabilized by moving back up a bit this week while Q1 2020’s data has not. The market decided (it seems thus far) to skip over the earnings weakness (an earnings shrinkage vs. the prior year) in Q2-Q4 2019 and look ahead to better times. They had better show up!

For Q2 2019, analysts are projecting earnings growth of 0.1% —> -1.3% -> —> -2.1% —> -2.6% -> -2.6% -> -3.0% -> -1.9% -> -2.6%-> -1.0% -> -0.7% -> -0.4% DONE

and revenue growth of 4.6% —> 4.3% —> 4.1% —> 3.8% -> 3.8% -> 3.7% -> 3.8% ->4.0% ->4.1% -> 4.1% -> 4.0% DONE

For Q3 2019, analysts are projecting earnings growth of 1.8% —> 0.8% —> 0.3% —> -0.5% —> -1.9% —> -3.6% -> -3.7% -> -3.8% -> -3.7% -> -4.1% -> -4.6% -> -4.7% -> -3.7% -> -2.7% -> -2.4% -> -2.3% -> -2.2%

and revenue growth of 4.4% —> 4.4% —> 4.2% —> 3.8% —> 3.2% -> —> 2.9% -> 2.8% -> 2.8% -> 2.8% -> 2.8% -> 2.7% -> 2.6% -> 2.8% -> 3.1% -> 3.2% -> 3.1% -> 3.1%

For Q4 2019, analysts are projecting earnings growth of 8.1% —> 7.5% —> 7.2% —> 6.3% —> 4.9% -> 4.5% -> 3.9% -> 3.5% -> 3.4% -> 3.2% -> 3.0% -> 2.9% ->2.6% -> 2.3% -> 1.5% -> 0.7% -> -0.4% -> -1.1% -> -1.4% -> -1.4%

and revenue growth of 4.8% —> 4.8% —> 4.6% —> 4.3% —> 4.0%-> 4.0% -> 4.0% -> 4.0% -> 3.8% -> 3.7% -> 3.6% -> 3.6% -> 3.6% -> 3.5% -> 3.2% -> 3.0% -> 2.6% -> 2.6% -> 2.5% -> 2.5%

For CY 2019, analysts are projecting earnings growth of 3.4% —> 3.2% —> 2.7% —> 1.7% —> 1.4% -> 1.3% -> 1.3% -> 1.3% -> 1.2% -> 1.1% -> 0.7% -> 0.6% -> 0.3% -> 0.1% -> 0.0% -> 0.1%

and revenue growth of 4.7% —> 4.7% —> 4.5% —> 4.4% —> 4.3% -> 4.2% -> 4.1% -> 4.1% -> 4.1% -> 4.1% -> 4.0% -> 4.0% -> 4.0% -> 4.0% -> 3.9% -> 3.8%

For Q1 2020, analysts are projecting earnings growth of 10.5% —> 9.8% —> 8.5% -> 8.2% -> 8.1% -> 7.9% -> 7.9% -> 7.8% -> 7.6% -> 7.3% -> 6.7% -> 6.0% -> 5.6% -> 5.3% -> 5.1% -> 5.3%

and revenue growth of 6.2% —>5.8% —> 5.6% -> 5.7% -> 5.5% -> 5.5% -> 5.4% -> 5.4% -> 5.5% -> 5.3% -> 4.8% -> 4.7% -> 4.5% -> 4.5% -> 4.5% -> 4.4%

For Q2 2020, analysts are projecting earnings growth of 13.3% —> 13.5% -> 12.0% ->12.6% -> 10.7 -> 9.9% -> 9.3% -> 9.2% -> 9.1% -> 9.0% -> 9.0% -> 8.7% -> 8.6% -> 7.7% -> 7.3% -> 6.7% -> 6.6% -> 6.4% -> 6.7%

and revenue growth of 6.8% —> 6.6% -> 6.7% ->6.6% -> 6.5% -> 6.4% -> 6.5% -> 6.4% -> 6.4% -> 6.3% -> 6.3% -> 6.3% -> 5.9% -> 5.2% -> 5.2% -> 4.9% -> 5.0% -> 4.9% -> 4.9%

For CY 2020, analysts are projecting earnings growth of 10.7% -> 10.6% -> 10.6% -> 10.6% -> 10.5% -> 10.6% -> 10.4% -> 9.9% -> 9.8% -> 9.7% -> 9.7% -> 9.9%

and revenue growth of 5.6% -> 5.6% -> 5.6% -> 5.6% -> 5.7% -> 5.6% -> 5.3% -> 5.3% -> 5.3% -> 5.4% -> 5.5% -> 5.5%

The earnings and revenue data was already discussed above!

Here’s a Brief Review of the Other Market Risks at Hand:

China Deal Risk: No Change. The overall market has ignored it. We are told a deal is imminent, and then it is not. The Chinese are gaming Trump, and he’s not folding, but he’s bending and says he will make a series of deals, including a first deal that may look light on results. Xi has the edge as “Lifetime Leader.”

Fed Rate Cut/Hike Risk: The Fed has cut three times and said it was done unless things get worse for the economy. Now the probability is 0% for a 4th cut in mid-December as assessed by CME Group. The risk was 22.1% 4 weeks ago. The risk of a rate HIKE is 6.6% now vs. 0% last week.

As I’ve said previously: “THREE cuts is a mid-cycle adjustment. Four cuts or more mean the Federal Reserve expects a recession.” A hike in rates in the near future would tank the U.S. stock market.

What about January? The odds of cut #4 is 12.4% vs. 13.9% last week vs. 35.8% two weeks ago vs 67% six weeks ago! The odds of a HIKE in Jan. are 5.8%.

What about March? The odds are 23.3% vs. 25.3% last week vs. 75.1% six weeks ago for 4 or more cuts in total. March hike? 5.0%.

April Cut? 34.8% vs. 52.6% last week vs. 79.7% 6 weeks ago expect there to be 4 or more cuts. April hike? 4.2% odds.

June cut? 43.5% vs. 43.6% last week vs. 56.7% 3 weeks ago expect four or more cuts by then. Probability of a hike is 3.6% vs. 10.2% last week vs. 0% 2 weeks ago.

July? 49.4% vs. 48.2% last week 60.7% 3 weeks ago expect 4 cuts by then. A hike? 3.2% vs. 9.2% last week.

What are the rest of the available “4 cut odds”? Sept. 2020? 58.9% vs. 53.2% last week vs. 38.7% 2 weeks ago vs. 65.2% 3 weeks ago. Sept. 2020 Hike? 2.6% vs. 8.1% last week. Nov. 2020 cut: 62.9% vs. 57.3% last week vs. 41.6% 2 weeks ago vs. 69.3% 3 weeks ago. Nov. hike? 2.3% vs. 7.2% last week. Dec. 2020 Cut: 66.5% vs. 61.7% last week and 73.8% 3 weeks ago. Dec. hike? 2.1% vs 6.3% last week.

In sum, the risk of another rate CUT (recession risk goes up) is above 50% first in Sept. 2020 vs. in April last week and continues through December with the odds increasing into 2020 year end. The risk of a HIKE bizarrely starts in December 2019 (not happening IMO), but the probability of a hike fell for 2020 to the low single digits from last week. Rate cuts are being pushed out while rate hikes are considered a bit less probable for the entirety of 2020.

SAME: For now, that means a majority of investors believe that recession is on the schedule for 2020, or at least the conditions that will force the Federal Reserve to act to avoid recession or make it a more shallow one. That means they are ultimately worried about what I call a “Big Bear Market“ (click and scroll to definitions in blue under “New Rules”).

The Risk of a Neutral Fed: Same. Ultimately the change was NOT positive for the U.S. equity market, but it ignored it. The market is behaving as if it does not care about the Neutral Federal Reserve despite the fact that the President is pleading for more cuts as the market moved higher and now has stalled out.

Takeaway Point SAME: The Federal Reserve is not just “in Neutral,” it’s politically STUCK IN NEUTRAL! (or it will be perceived the Fed is political and anti-Trump – something you have not heard from the mainstream media – their narrative is that Powell is independent of Trump.)

My Investing Scenario shifts a bit this week….

Current Scenario…(modified from prior)

Trading or even adding except doing so blindly by calendar or automated purchases here is tricky. Even if the market pops a bit as soon as Monday, the prior pattern we saw earlier this year could repeat itself (up slightly off a long consolidation and then down sharply into a mild to moderate correction [5-15%]). The market could continue higher however if the trade deal is better than thought and/or if the Congress moves to censure or admonish Trump vs. impeach him (he will spin ANY of that to his advantage). A final high will be reached prior to the discounting of a recession, which brings on a ‘Big Bear Market.’ Whether the market moves up a bit and cracks back, corrects immediately, OR rises now to a final (for the cycle) all time high, we are not yet at the all time high yet. Got it? 😉

Bottom Line: I am holding my current exposure for now and seeking markets outside the U.S. to add back exposure other than to trim off the exposure represented by my most recent adds (bought some CBRE, EWG, and XLE and sold SPY). Why? Because I’m overexposed to the US market at this point in allocation terms, and I would favor a correction from this level before the final all time cycle high is reached. Yes, global markets could fall too, so I’m moving in steps to “buy foreign.” If we don’t see a U.S. market drop, there are other markets to buy without chasing a market I am already overexposed to.

U.S. Iran War Risk: No change this week. More stable after the leak of the “Iran Annihilation Plan HERE.

2020 Election Risk: The Democrats were unable despite compelling testimony that Trump did something wrong (Newsbreak: He did) to move public opinion toward conviction. Without that, impeachment may look like a game they are playing and people don’t like games, even if justified at some level. “They are wasting our time” is the thought.

Why is this happening? Because although Trump et. al. were knee deep with Russia in 2016, they did not engage in an organized conspiracy to work with them. They just bumbled around in a way that made it necessary for the FBI to investigate. If you were to meet with key Russians over and over, they would investigate you as well. The idea that they should not have been doing surveillance is ignorance of reality in my view.

Mueller showed clearly the Russians interfered substantially in our election process in 2016. Trump doesn’t like to admit that because it hurts his “poor baby ego.” Bottom line? Trump can use this to assert that because they blamed him for direct collusion, which was unproven, the Ukraine “Drug Deal” as Trump’s own NSA chief Bolton called it, was all the same thing. It wasn’t, but his illogic will persuade the poorly informed public, and he’ll have a good shot at re-election considering the disarray and far left leanings of the Democrats.

Biden still has to win the Dem nomination for the Dems to win in 2020 IMO. Bloomberg won’t activate the Dem base as a billionaire who ran stop/frisk ops in NYC as much as it made the city safer. The Democrats are actively weakening their best chance, because they are leaning too far left. They make fun of Biden, who is a mostly cured, but not entirely cured stutterer, which he has shared before but not widely until a recent article came out. So try to be kind if he has trouble getting a word out! Unless you are perfect of course… 😉 I don’t like all his policy choices, but I do respect his work on behalf of our country.

Warren and Sanders are too controlling for voters to fully embrace as they did Obama. “Medicare for Everybody Who Doesn’t Want It” is their motto or shove it! We Americans don’t like that except for the elites on the far left that do not want the private sector to compete against Medicare. Let them compete I say! The winner(s) will be selected based on price and quality! (Biden is missing this point in his defense of “Medicare for All Who Want It.” I say it’s an “American argument.”)

Trump Impeachment Risk: Little change but possibly slightly lower. See above. Conviction Risk? Near zero.

Deficit/Debt Threat: No Change: Trump is now beating Obama at something! The size of his deficit! Read THIS. The deficit is up 26% to $964 Billion for fiscal 2019, the HIGHEST IN 7 YEARS!

I’ll leave this here as a monument to our monumental debt, which could threaten interest rates in the future. When rates rise, there will be “heck to pay.” The U.S. dollar remains at risk and having at least 5% gold exposure is a reasonable hedge in any portfolio. Some say higher, but owning stocks is also a hedge that over time would work out for solid companies, even in the face of very high inflation (not in the case of bankruptcies of course!).

Back to the charts….

Now take a look at the SP500 chart. The green line is 2940.91, the

9-21-2018 High preceding the decline ending December 24th. The long upper yellow line is now at about 3062 at the Friday close. The two short upper red lines show a narrow range in a gentle up trend, rising ABOVE the prior upper trend line.

As I warned two weeks ago, if the market keeps pushing above that top yellow line (the longer one), there will be an eventual payback.

SP500 Large Cap Index (click chart to enlarge; SPX, SPY):

Time for a move!

Now let’s check in on two “Canary Signals” we’ve been following:

“Intel-igent Market Timing Signal” (Intel; I*NTC; * there to throw off the crawlers!): Neutral. SAME: “The stock is stuck below the April ATH. Why should it break out if the U.S. GDP is due to slide to below 1%? Think about that. The June 4 high of 57.60 has been exceeded, and the April high of 59.59 is the next test to achieve a new all time high.”

Bank of America (B*AC) Market Timing Signal: Bullish, but needs to push higher soon. There has been 1 close above 33.05, which was the early 2018 high (I quoted a slightly lower number before as I apparently picked out a slightly lower high in that time frame). This is a major breakout if it holds. It will only hold if rates keep climbing. Sell a reversal at least on a close or sell on a close with higher volume IMO.

Keep up-to-date during the week at Twitter and StockTwits (links below) where a combined 34,144 investors are following the markets with me…

Follow Me on Twitter® Follow Me on StockTwits®. (real time messages are ONLY on StockTwits until Twitter reforms its policies, but we’ll have it as a backup system)

Join the Conversation in the StockTwits “MarketTiming” Room

Now let’s go on to review investor sentiment…

Survey Says!

Sentiment of individual investors (AAII.com) showed a Bull minus Bear percentage spread of +5.21% vs. +15.90%. Sentiment should be peaking if this is in fact a top. It is not a top. It could be a temporary top, but it’s not “The Top.” Follow the direction of the next move and prepare to be disappointed if it’s up (see above).

| Bulls | Neutrals | Bears |

| 34.24% | 36.72% | 29.03% |

| Thurs. 12 am CT close to poll | ||

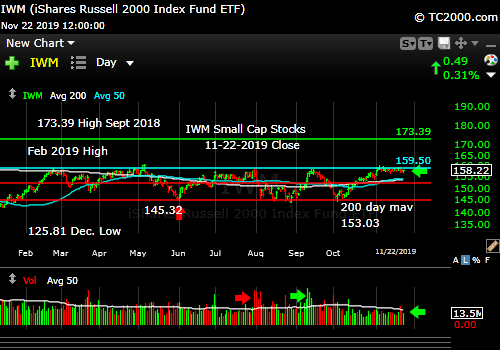

2. U.S. Small Caps Market Timing (IWM):

Same: But now 15 days without a breakout as noted above. “Bad sign that IWM could not break out with the large caps continuing their climb or even match the midcap breakout. If you see a breakout, it will be a positive sign for at least another Bullish stretch (for large and midcaps too) before the next decline.”

Russell 2000 U.S. Small Cap Index (click chart to enlarge; IWM, RUT):

Stagnant! Follow the next move.

3. Gold Market Timing (GLD):

No change.

SAME: Things are shifting… We’ve gone from “recession risk” and “multiple cuts” as well as “don’t fight the Fed” to “Three cuts and done.”

SAME MAJOR POINT: IF the Fed lags inflation, gold wins, but if it front runs inflation, gold loses on a relative basis. My contention as said above is that Federal Reserve bias will now be against raising rates prior to the election, so inflation will get a boost! Gold wins…but it must perform on the charts to prove it!

Technicals: Gold is just below that key top red line, and slightly above the 2013 lower high. If it breaks and GDX breaks, I’ll likely be lowering my exposure to gold. Holding above that 2013 lower high on the chart…for now.

The Gold ETF (click chart to enlarge; GLD): That top red line is 137.80.

Gold on the edge of a move too.

4. Interest Rate Market Timing (10 Year Treasury Yield; TNX, IEF, TLT):

SAME: As long as the Federal Reserve stays “Neutral,” rates will be rangebound barring a left field event, a.k.a. a “Black Swan event.” Lower rates imply the Fed medicine is not working yet/ever. I believe it’s a waste of time to lower rates except as a temporary goosing of the economy, and it has a negative impact on savers and on inflation (raises inflation due to down dollar). I don’t like either of those. It hurts the poor most of all as they don’t own stocks or real estate. They don’t even get the positive feedback that it’s good to save money in the bank.

Check out the “Market Signal Summary” below – after you review the following chart…

U.S. 10 Year Treasury Note Yield (click chart to enlarge; TNX, IEF, TYX, TLT, TBF):

Rates down but in short term up trend at the moment.

Now let’s review three key market timing signals together….

Do not use these signals as a trading plan. They are rough guidelines. I currently share my BUYS and SELLS in as timely a way as possible on social media (links above).

MY MARKET SIGNAL AND TREND SUMMARY for a Further U.S. Stock Market Rally with Real GDP Growth (“Real” means above inflation):

Stock Signal YELLOW for a further U.S. stock market rally with a longer term Bullish and short term Bullish SP500 Index trend. The stock signal is based on small caps, as they often lead the market down. SAME 11-22-19: Small caps are barely moving. The top was established on Feb. 25th. Above there, the Bull will be back in full swing.

The VIX Score will be shown in the context of Bull Market Health Score above to avoid redundancy.

Gold Signal YELLOW for a further U.S. stock market rally longer term Bullish Trend and a short term NEUTRAL Gold Trend. The current pattern is a warning sign. The longer term Bullish trend will evaporate if it breaks below the current level by much at all.

What gold does mostly as I’ve written HERE is follow real interest rates around the world (if you own “gold in dollar terms” you care about U.S. rates most of all). The rest of the world does matter however, including massive buying by central banks.

Remember, gold may be down but not yet out, because if the Fed lags inflation, gold will win. Since I am predicting a “lagging Federal Reserve” into the 2020 Election, inflation will win, and gold and oil will win.

From before: “Remember GLD is being used as an indicator for the ECONOMY here.” If gold continues to rise, it means the market believes real rates will fall, which in the current context means the global economy is slowing. That would ultimately hurt U.S. stocks.

Rate Signal YELLOW for a further stock market rally with a longer term BEARISH and short term Bullish 10 Year Yield Trend. (Remember: higher rates mean lower bond and Treasury prices). Whether the short term trend should be called Neutral vs. Bullish is arguable at this time, but it’s not Bearish yet. There is actually an even longer term view that says rates have been in a neutral trading pattern since 2011, but the above two views are more practical on a trading/intermediate term investing basis.

I’ll leave this reminder from 9-20-2019’s issue: “Remember, FOUR Fed cuts will NOT be a “mid-cycle adjustment” and would be taken badly by the market ironically, considering the market’s addiction to lower rates. A fourth cut means the Federal Reserve is seeing recession risk as significantly high.”

Also for Reference: “Rates usually RISE slowly in a strong recovery and the stock market rally continues as they rise, as I’ve repeated multiple times on social media and here. Empirically though, rates that are “lower” (than 3.11%) and are NOT rising rapidly have allowed the market to rise.”

I said weeks ago, “Watch the oil price too. Higher oil tends to mean higher rates.” It closed at 57.77 vs. 57.76 last week vs. 57.24 the week before. Still holds: If it rises above 58.82 and then 60.94, oil and oil stocks will be off to the races. 63.38 would be the next target. Since May, the price of oil almost appears to have been managed to stay between 50 and 59/barrel. I wonder why? 😉

Just a reminder: If TNX bounces too quickly and too high, this will give rise to Rate Shock III… As said before: “Watch the rate at which TNX climbs if the current trend reverses. If it shoots up very fast, stocks will correct.” In the Sept. 28th issue: “A rapid push higher in rates would mean trouble for stocks, as occurred in early 2018. That’s what I called ‘Rate Shock.'” I called the period of rising rates in early October #RateShockII.

Another Reminder: “The risk lately has been ‘Falling Rate Shocks.’ (I changed the term from “Negative Rate Shocks” because there are in fact negative rates in a lot of countries now. First we had ‘Falling Rate Shock I’ in December 2018 (because rates FELL while the Fed raised the Fed Funds rate 0.25% in mid-December, in what was perceived as a policy error by critics), ‘Falling Rate Shock II’ in May, and ‘Falling Rate Shock III’ in August. The Stock Market Bulls had better hope that they don’t get more rate cuts past October.

Thank you for reading. Would you please leave your comments below where it says “Leave a Reply”… or ask a question or report a typo…

Pay it forward by sending the link to MarketTiming.Blog (that link will immediately connect them to this webpage) to a relative or friend. Thanks for doing that.

Be sure to visit the website for more general investing knowledge at:

Standard Disclaimer: It’s your money and your decision as to how to invest it.

I thank Worden Brothers for the charting system I use to post these charts. If you want to know more about the charting system I use every day, contact me. It makes it much easier to follow along with me if you can see the charts and manipulate them on your own computer. It’s a great investment to have an excellent charting system.

Note: I’ve updated my criteria for the equity signal for a further U.S. stock market rally to the following: GREEN = Bullish, YELLOW = Neutral, RED = Bearish. In other words, the colors tell you whether the signal supports the stock rally or not, while the Bullish, Neutral, and Bearish designations are about the trend.

A BEARISH trend signal does not mean we should not buy. A BULLISH trend signal does not mean you cannot sell some exposure. It depends on what is going on in the economy and how oversold/overbought the market is at a given point whether the Bearish signal is to be sold or bought, sold on the next bounce, etc. and whether a Bullish signal is to be bought or if profits should be taken. A NEUTRAL trend signal does not mean the end of the Bull or Bear. It means to wait and look for possible subsequent entry points within the existing trend, Bull or Bear, but preserve capital if the entry fails. Our strong intention is to buy low and sell high. By the way, I will keep showing the prior orange “Trigger lines” in the IWM and GLD charts for now as reference points only; they have historical value for us from the post-2016 election period.

Copyright © 2019 By Wall Street Sun and Storm Report, LLC All rights reserved.